Lanvin Group has another party betting on its success. In the wake of Meritz Securities Co. committing $50 million in a private placement ahead of Lanvin Group’s NYSE listing this month, the Shanghai-based fashion group announced on Monday that Handsome Corp. – which has been the exclusive distributor of the Lanvin brand in South Korea since 2007 – will join the roster of strategic investors participating in its impending merger with blank check firm Primavera Capital Acquisition Corporation (“PCAC”). Lanvin Group said this week that it expects the $1 billion business combination to close “shortly after shareholder approval,” subject to customary closing conditions.

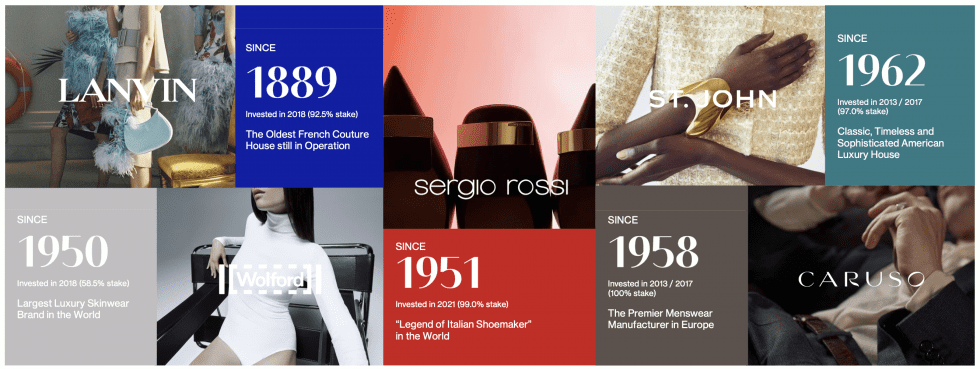

“Chances are good that shareholders will approve the deal” during PCAC’s extraordinary general meeting on December 9, according to a recent note on Seeking Alpha, “paving the way for Lanvin Group to meet its previously promised deadline to become publicly listed by year-end.” In an email on Tuesday, Lanvin Group – which consists of Lanvin, footwear brand Sergio Rossi, knitwear company St. John, hosiery-maker Wolford, and menswear company Caruso – alerted TFL that its listing is slated to take place on December 15. It will trade under the LANV ticker symbol.

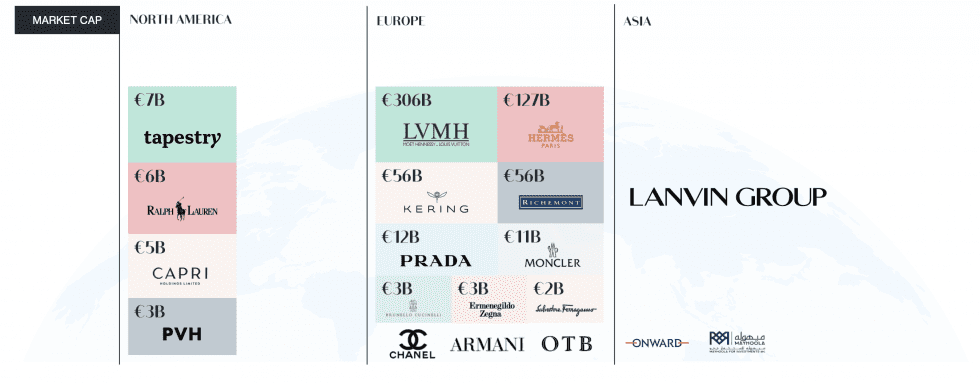

As for what the future holds for Lanvin Group, the public listing “will only be the start of a much longer journey,” with the group expected to face “challenges carving out a place in the crowded global luxury goods industry,” the SA note states. In other words, it will likely be an uphill – and expensive – battle for Lanvin Group to amass market share in the luxury segment, which is currently dominated by the likes of LVMH, Richemont, and Kering.

The group’s marquee name Lanvin has seen a string of executive and creative shakeups in recent years, including former CEO Jean-Philippe Hecquet, who left in 2020 after just 18 months in the role. At the same time, other brands, including St. John and Wolford, for instance – which “are known for durable, quality fabrics but suffer from fusty images,” as Quartz’s Tiffany Ap put it this fall – need “significant work” from a consumer perception standpoint. This might be difficult in light of Lanvin Group’s overall lack of luxury expertise; after all, the group falls under the umbrella of Fosun International, a Chinese conglomerate best known for its financial, real estate, steel, and healthcare businesses.

Facing Challenges, Looking to China

These challenges are not lost on Lanvin Group, which has been engaged in an expansive overhaul ahead of the public listing. One of the first major signals of change came in October 2021 when Fosun Fashion Group announced that it would rebrand to Lanvin Group, which it characterized as “a clear statement of the [its] intent to build a global portfolio of iconic luxury fashion brands.” Since then, the company has not been shy about its ambitions to rival luxury’s most established conglomerates with a group of its own.

One need not look further than the group’s announcement of the SPACback in March, in which it touted its “strong foundation in Europe combined with a unique position to capture significant growth opportunities in the world’s largest luxury markets – North America and Asia, where the Group has built an extensive luxury fashion ecosystem.” Specifically, Max Chen, Chairman of PCAC, and Partner of Primavera, the Chinese investment firm launched by Fred Hu, former chairman of Greater China at Goldman Sachs, stated at the time that Lanvin Group boasts “a differentiated strategy to build a luxury powerhouse for a new generation of consumers, especially benefiting from surging luxury consumption in Asia.”

Not overlooking the importance of the American market, the latter element – luxury consumption in Asia and China, in particular – appears to be the key to Lanvin Group’s future. In an investor presentation released in November, Lanvin Group emphasized the “significant growth opportunities” in Greater China, and its ability to act as an “unparalleled” pipeline to “the largest and fastest growing luxury market in the world” by virtue of it being the first and only global luxury group headquartered in China. Specifically addressing its plans to leverage its capabilities in China, which is expected to become the world’s largest luxury market by 2025, Lanvin Group stated in the presentation that it has a “360° brand operation by local team, support from strategic partners, dedicated content and product offerings, and online and offline expansion [opportunities].”

For a snapshot: Lanvin Group mentions “China” some 50 times in the deck – compared to 6 mentions of EMEA, 13 mentions of America, and 6 mentions of the European market.

Still yet, other changes have come into fruition: This spring, Lanvin Group entered into a partnership with Shopify to build a North American digital platform powered by the e-commerce company’s technologies. “Lanvin and Sergio Rossi will become the first of the Group’s luxury brands to transition onto the digital platform in the North American market,” the group revealed in April, “allowing them to unlock new growth opportunities with market-leading digital capabilities in the world’s largest luxury fashion market.” Speaking about the Shopify partnership in April, Lanvin Group chairman and CEO Joann Cheng, Chairman and CEO of Lanvin Group, said that the group’s “legacy-light and digital-native model allows us to integrate Shopify’s disruptive technologies across our portfolio of heritage brands,” making it “even better equipped to capture the significant growth opportunities we have identified in North America.”

At Lanvin, in particular, change is similarly afoot. The swapping in and out of C-level figures appears to have stabilized to an extent under creative director Bruno Sialelli. (Lanvin Group chairwoman and CEO Joann Cheng is still in the interim CEO role at the brand.) While Lanvin does not appear to be rivaling its closest competitors when it comes to buzz worthiness, under the watch of Sialelli, it is bulking up its accessories offerings; the brand, which maintains the title of the oldest French fashion house in operation, has lacked the robust arsenal of accessories (often emblazoned with recognizable logos and/or monograms) that enable big, conglomerate-owned fashion brands to generate revenues reaching into the billions. And its revenues are on the rise. During the first half of the year, Lanvin’s sales rise by 117 percent to 64 million euros ($63 million), a nod to what management says is “the brand’s growing appeal and [its] strong demand among luxury fashion buyers.”

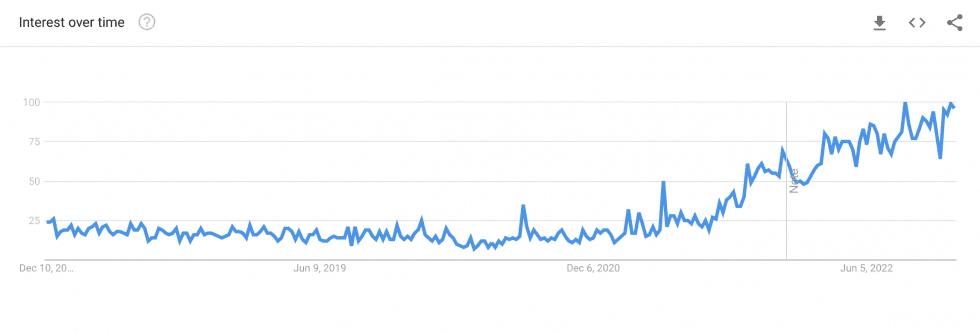

It is also worth noting that Lanvin is trending upwards in terms of Google searches in the U.S.; there is a very good chance, of course, that such searches are being boosted by the impending Lanvin Group IPO.

Meanwhile, Sergio Rossi – which Lanvin Group snapped up in July 2021 – has a new creative director, four new outposts in China, and benefits from the Shopify deal by way of new e-commerce capabilities in the U.S.

Cheng says she is confident about the future of the group, citing room for growth on a global scale. The American market is responsible for approximately 15 percent of sales for the Group, with the potential for “at least” 10 percent more growth, and growth of nearly 30 percent can be expected in Greater China, which currently represents 14 percent of sales. And shedding light on ambitions on the M&A front, Cheng asserted in connection with Lanvin Group’s first-half report in Octoberthat the group is actively looking at “new luxury brands,” namely, those that target Gen-Z consumers and/or brands with a “relatively new business model and a strong online presence.”

THE BIGGER PICTURE: Lanvin Group’s impending listing follows from earlier IPOs of Chinese titans like Alibaba, JD.com, Baidu, and Pinduoduo, among others, which have been drawn to U.S. as “the home of the world’s largest and most liquid stock market,” according to University of Rochester Simon Business School professor Joanna Wu, who notes that “listing in the U.S. ‘bonds’ a foreign company to America’s stringent litigation and regulatory environments, sending a favorable signal to investors about a company’s quality.” She also states that “a peculiar feature of China’s stock market is that only profitable firms are qualified for listing,” thereby, driving some promising but not yet profitable Chinese firms – like Lanvin Group, which is not projecting profitability until 2024 – “to seek overseas listings, especially in the U.S., because they are ineligible to list at home.”

Not without issues, some Chinese companies that already listed on U.S. exchanges have found themselves in the crosshairs of a longstanding auditing dispute between U.S. and China regulators, with big names like Alibaba having faced risks of being delisted from American exchanges. Wu states that in addition to scrutiny from regulators in the U.S., “the Chinese government has also come down hard on U.S.-listed Chinese companies,” which saw the “last-minute cancellation in 2020 by Chinese regulators of Ant Group (an affiliate of Alibaba Group)’s Hong Kong IPO, Chinese regulatory sanctions imposed on Didi Global within a week of its New York IPO in 2021 for cybersecurity reasons, and the recent crackdown in 2021 by the Chinese government on the private tutoring sector.”

Regulators in the U.S. and China reached an initial agreement this summer to help resolve their auditing clash, prompting speculation that roughly 200 Chinese companies listed on U.S. stock exchanges will avoid being removed and that a “pretty strong pipeline” of Chinese companies that want to list on U.S. exchanges in “the coming months” might come into fruition following a striking drop in new listings of Chinese companies in the U.S.

– The Fashion Law

Leave a Reply